Rocket Lab is an end-to-end space company that earns revenue from launch services, spacecraft manufacturing, satellite components, mission operations, and related space systems work. Its model combines mission-based launch contracts with longer-duration spacecraft and defense programs, plus component sales to satellite manufacturers and government customers.

The company reports two operating segments

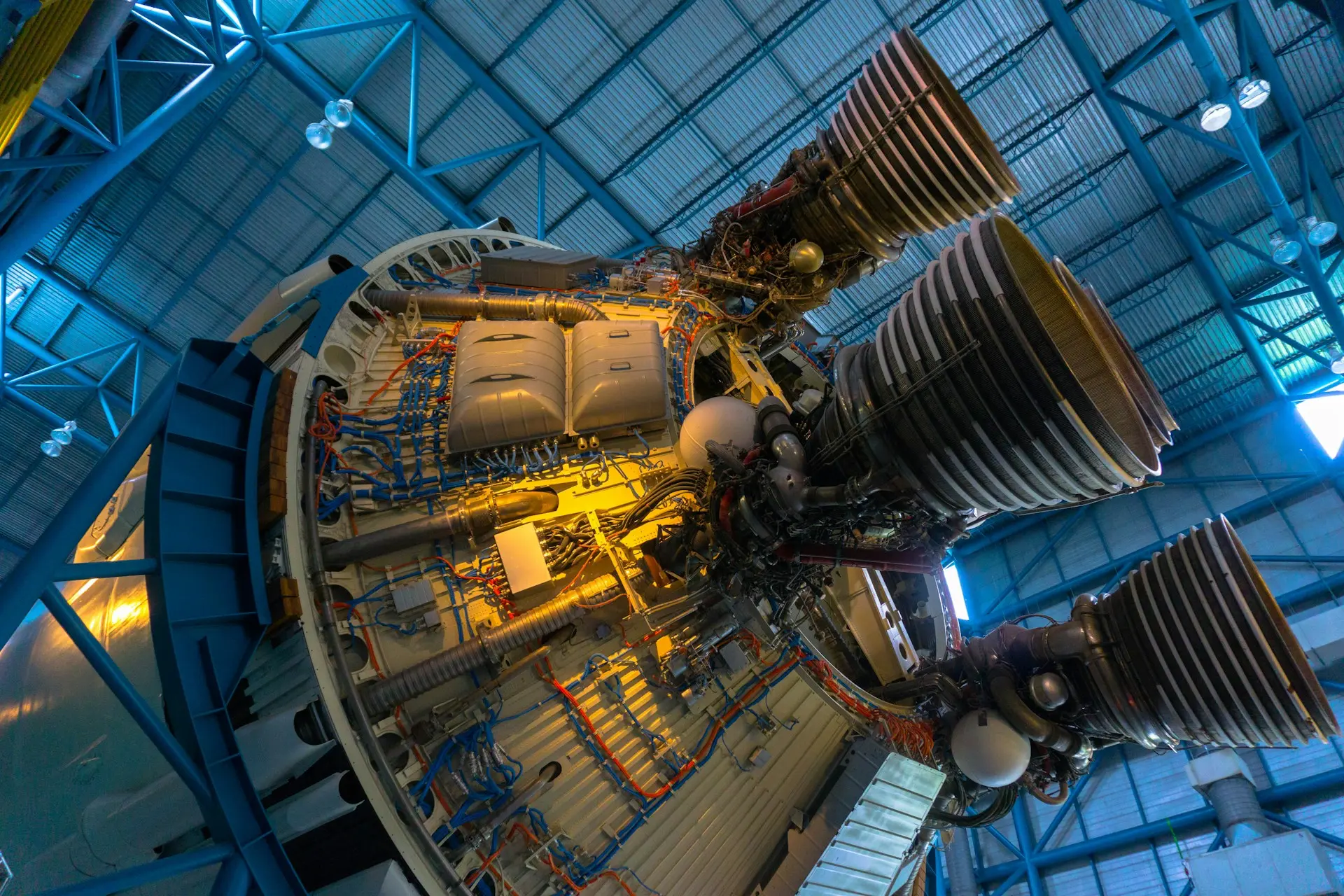

- Launch Services: Designs, manufactures, and launches orbital rockets for dedicated missions and rideshare customers. This segment includes Electron, the established small-launch vehicle, HASTE for hypersonic suborbital test missions, and future Neutron launch services.

- Space Systems: Supplies spacecraft, satellite components, program management, mission operations, optical systems, command-and-control software, batteries, solar solutions, reaction wheels, star trackers, radios, separation systems, and related technologies.

In Q1 2026, Rocket Lab generated $200.3 million of revenue, up 63.5% year over year. Space Systems produced $136.7 million, or about 68% of revenue, while Launch Services produced $63.7 million, or about 32%. This mix shows that Rocket Lab has moved beyond a pure launch-service model into a broader role as a spacecraft and mission infrastructure supplier.

Revenue comes from fixed-price launch and spacecraft-build contracts, long-term government and defense programs, and purchase-order-based component sales. Recognition varies by contract, with some revenue recorded over time as work is performed and some recorded at delivery or launch.

Rocket Lab’s strongest market position is in small orbital launch and vertically integrated space systems. The company describes Electron as the world’s most frequently launched orbital small rocket and said Electron was the second most frequently launched orbital rocket in 2025. Through March 31, 2026, Rocket Lab had completed 81 successful missions, including suborbital launches, and delivered more than 200 spacecraft to orbit.

The company’s competitive advantages include

- Vertical integration: Rocket Lab controls launch vehicles, spacecraft platforms, components, software, mission operations, and selected optical and robotics capabilities.

- Proven launch cadence: Electron has an established flight record in a market where reliability and schedule availability are major customer concerns.

- Private launch infrastructure: The Mahia, New Zealand launch complex gives Rocket Lab more schedule control than launch providers dependent only on shared government ranges.

- Defense alignment: HASTE, missile-defense work, Space Based Interceptor support, and Space Force satellite production place Rocket Lab in areas tied to U.S. and allied national-security spending.

- Expanding component heritage: Rocket Lab flight hardware and spacecraft components have flown on more than 1,800 missions, supported by acquisitions including Sinclair Interplanetary, Advanced Solutions, Planetary Systems Corporation, SolAero, GEOST, Mynaric, and Motiv Space Systems.

Backlog supports the company’s market position. At March 31, 2026, Rocket Lab had $2.22 billion of backlog, up from $1.85 billion at year-end 2025. Space Systems accounted for $1.30 billion of backlog and Launch Services accounted for $921.4 million. Its launch manifest exceeded 70 contracted missions after 31 new Electron and HASTE contracts and five new dedicated Neutron launches were signed during Q1 2026.

Direct competitors include SpaceX in launch and broader space services, plus emerging U.S. and international small- and medium-launch providers. In satellite systems and components, Rocket Lab competes with spacecraft manufacturers, defense primes, subsystem suppliers, and specialist component vendors.

Compared with SpaceX, Rocket Lab is far smaller and less capitalized, and it does not yet compete at the same scale in heavy launch or large constellation ownership. Its differentiation is narrower but clear: frequent dedicated small launches through Electron, a growing spacecraft and component business, and a strategy to expand into medium lift through Neutron. Neutron is important because it would move Rocket Lab into larger constellation, national-security, civil space, and exploration missions.

China is not a meaningful disclosed direct market for Rocket Lab. The company lists operating subsidiaries in the United States, New Zealand, Canada, and Australia, with no China operating base or China-specific revenue disclosure. China still matters indirectly through space competition, export controls, sanctions, tariffs, and U.S. national-security procurement priorities.

.webp)